Top 3 Stocks Thriving in AI Boom and Future Growth

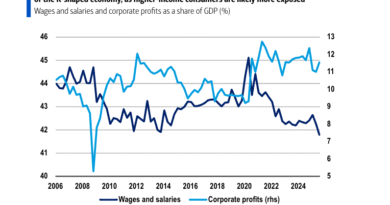

Equity markets worldwide are showing signs of increased vulnerability, with a heavy reliance on the United States, which itself is profoundly shaped by the ongoing AI surge. This leaves numerous investors overly dependent on one prevailing narrative. The enormous investments pouring into AI infrastructure are fueling the US economy, propelling stock market performance, and enhancing consumer spending via the wealth effect.

The dominance of US stocks and AI themes has led to highly concentrated and overvalued global equity markets. If this massive expenditure comes under scrutiny and is eventually scaled back—as anticipated due to unclear returns on capital—the repercussions could be substantial.

Artificial intelligence stands as a revolutionary technology poised to fundamentally alter economies, yet we contend that its full impact will unfold over many years. This implies that investors may be placing too much weight on immediate outcomes. Should the fervor surrounding AI diminish and capital spending be reduced, the current pattern favoring hardware over software could easily flip. From our perspective, such a shift presents a compelling investment opportunity.

Beyond the AI Surge: Three Reliable Stocks for Sustained Growth

Two standout companies that align perfectly with this outlook are Automatic Data Processing and Accenture. Automatic Data Processing, listed on Nasdaq under the ticker ADP, operates as a premium, defensive compounding business with a commanding presence in worldwide payroll and management software solutions. Its advantages stem from immense operational scale, profound knowledge of regulatory landscapes, and significant barriers to switching for clients, all of which foster predictable recurring income and exceptional customer loyalty. Key structural trends—such as the rise of outsourcing, growing intricacies in workforce management, and widespread cloud computing adoption—drive consistent mid-single-digit revenue expansion, rendering ADP particularly appealing for investors seeking long-term stability with minimal risk. We anticipate that ADP will actually gain from the integration of AI technologies, rather than being adversely affected.

Accenture, traded on the NYSE as ACN, holds a premier position in IT consulting and digital transformation services across the globe. It capitalizes on enduring structural drivers like the shift to cloud infrastructure, the uptake of data analytics and AI, heightened focus on cybersecurity, and corporate efforts to boost operational efficiency. With a cost structure that is predominantly variable, Accenture enjoys flexibility in maintaining margins across economic cycles. Moreover, its robust free cash flow generation enables reliable returns to shareholders through dividends and buybacks. The company’s proven execution capabilities and involvement in essential, non-discretionary expenditures position it as a superior long-term compounder. As AI permeates the global economy, we foresee it driving increased demand for Accenture’s offerings while enhancing profitability margins.

An additional enticing prospect, entirely independent of the AI narrative, is Novo Nordisk, listed on the Copenhagen exchange as NOVO-B. This innovative firm has pioneered treatments for obesity, yet its share price has plummeted by 70% over the past 18 months. We view this decline as driven by excessively negative assumptions regarding competition and pricing challenges, rather than any lasting damage to its core business.

Novo Nordisk maintains its solid position as the second-largest player in a highly promising, underserved global market for obesity treatments, which is projected to expand dramatically over the coming decade. The company’s valuation has dipped to just 13 times earnings at recent troughs—significantly lower than historical norms—despite delivering outstanding returns on capital and impressive cash flow production.

Recent changes in leadership, smart pricing strategies aimed at broadening patient access (especially with oral GLP-1 formulations), and a promising pipeline featuring next-generation candidates like CagriSema all point to a bright future. Current market sentiment and projections have diverged sharply from the underlying business strengths, establishing an ideal buying opportunity with substantial upside potential as growth stabilizes starting from 2027.