Can SanDisk Shares Make You a Millionaire Investor?

SanDisk’s Impressive Performance Since Spinoff

SanDisk (SNDK, down 0.96%) shares have delivered extraordinary returns to shareholders over the past year following its separation from Western Digital back in February 2025. A modest initial investment of $10,000 in the company at the time of the spinoff would have ballooned to approximately $131,380 today, representing a substantial multiplication of capital for those who got in early.

With such remarkable growth already achieved, many investors are now contemplating whether it is prudent to maintain their positions in SanDisk stock in expectation of additional appreciation. The firm’s earnings have been expanding at an astonishing rate, prompting some to view this as a prime artificial intelligence (AI) investment opportunity capable of generating transformative wealth, potentially turning modest portfolios into million-dollar fortunes.

In this detailed analysis, we will delve deeply into SanDisk’s future outlook, scrutinizing its market position, growth drivers, and valuation metrics to assess if it truly possesses the potential to deliver the kind of life-altering financial gains that investors dream of.

SanDisk’s Rally Fueled by Surging Market Demand

The blistering upward trajectory of SanDisk’s stock price shows no immediate signs of abating, supported by a robust market dynamic where customer demand for its core products far exceeds available supply. SanDisk specializes in manufacturing high-performance flash storage solutions that power a wide array of critical applications, including expansive data centers, personal computers, and mobile smartphones.

In particular, the company’s solid-state drives (SSDs) have become highly sought after, especially among operators of AI data centers. These facilities require vast storage capacities to handle the enormous datasets necessary for training sophisticated large language models (LLMs) and executing real-time inference tasks. The insatiable appetite for NAND flash storage—the key technology underpinning SanDisk’s offerings—has created persistent supply shortages projected to extend well beyond 2026.

This supply-demand imbalance underpins a favorable pricing environment for NAND flash that appears set to endure for the foreseeable future. According to insights from market research specialists at TrendForce, NAND flash prices are poised for a sharp escalation of 55% to 60% in the current quarter alone. Furthermore, projections from Bank of America analysts point to a robust 45% year-over-year increase in NAND flash revenues for 2026, propelled by a healthy 26% rise in average selling prices (ASPs).

However, these conservative estimates may understate the actual price surges, given the aggressive spending by major tech firms—pouring hundreds of billions into data center expansions—who are prepared to pay steep premiums to secure essential storage components from suppliers like SanDisk. It comes as little surprise, then, that reports indicate SanDisk has already doubled the prices on its 3D NAND enterprise SSDs this quarter, capitalizing on overwhelming demand from hyperscale cloud providers.

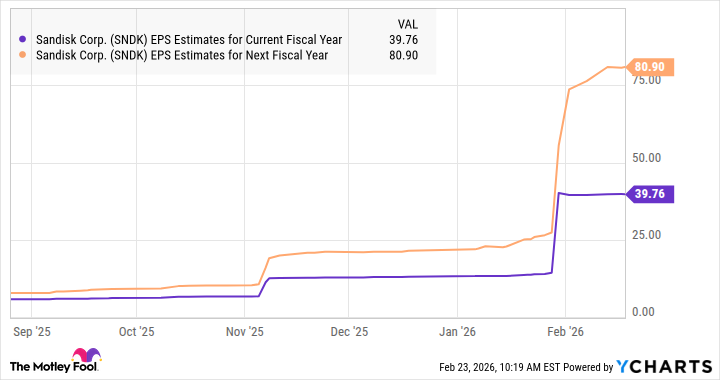

These dynamics position SanDisk for a dramatic expansion in profitability. Analysts anticipate the company’s earnings per share to surge dramatically from the prior year’s figure of $2.99, reflecting the potent combination of volume growth and pricing power.

Data courtesy of YCharts.

Assessing the Millionaire-Making Potential of SanDisk Stock

While the allure of a single stock promising millionaire status is undeniably tempting, basing an entire investment strategy on such high hopes carries inherent risks and is generally not advisable. Any slowdown or disruption in the AI infrastructure sector could swiftly derail SanDisk’s impressive momentum. Therefore, financial prudence dictates constructing a diversified investment portfolio to mitigate such vulnerabilities.

That said, incorporating SanDisk into a well-balanced portfolio could meaningfully contribute to long-term wealth accumulation goals, including reaching millionaire status over time. The stock’s current valuation remains attractively low at just 16 times forward earnings—a discount compared to the technology-heavy Nasdaq-100 index’s forward P/E ratio of 25.

Looking ahead, consensus forecasts illustrate a potential earnings per share of $80.90 by the following year, as depicted in the chart provided earlier. Should SanDisk’s shares eventually align with the Nasdaq-100’s forward earnings multiple, the stock price could more than triple from its present level of around $632.38. This scenario underscores that significant upside potential may still exist, making it far from too late for discerning investors to establish or add to their positions.

SanDisk’s strategic positioning within the explosive AI storage market, coupled with its undervalued metrics and constrained supply environment, suggests the company is well-equipped to sustain its growth trajectory. Investors eyeing substantial returns should weigh these factors carefully, always within the context of broader portfolio diversification to manage risks effectively.

The combination of escalating demand from AI-driven data centers, supportive pricing trends, and a compelling valuation paints a bullish picture for SanDisk’s future performance. As the company capitalizes on these tailwinds, it stands out as a noteworthy contender in the semiconductor and storage sectors, with the capacity to reward patient shareholders handsomely in the years ahead.